If a balance sheet date intervenes between the declaration and distribution dates, the dividend can be recorded with an adjusting entry or simply disclosed supplementally. Furthermore, as is evident from the statement in the General Electric Company annual report, a firm has other uses for its cash. Most mature and stable firms restrict their cash dividends to about 40% of their net earnings. sales invoice template In fact, dividends are not paid out of retained earnings; they are a distribution of assets and are paid in cash or, in some circumstances, in other assets or even stock. The announced dividend, despite the cash still being in the possession of the company at the time of the announcement, creates a current liability line item on the balance sheet called “Dividends Payable”.

- Whether you follow GAAP or use cash-basis accounting, you can make sure your financial reports are accurate with proper dividend reporting.

- In fact, dividends are not paid out of retained earnings; they are a distribution of assets and are paid in cash or, in some circumstances, in other assets or even stock.

- This entry is made at the time the dividend is declared by the company’s board of directors.

- Many investors view a dividend payment as a sign of a company’s financial health and are more likely to purchase its stock.

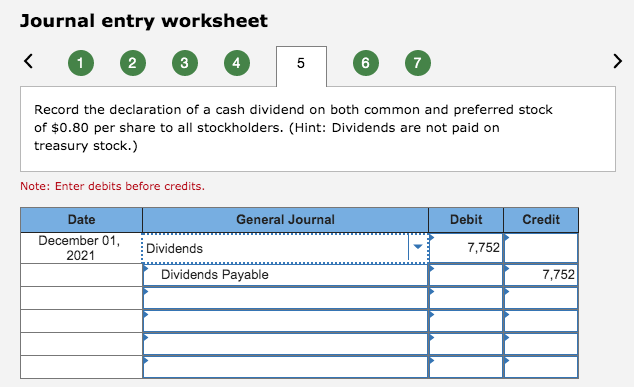

Cash dividend journal entry

Whether you issue dividends monthly or choose to only issue dividends following a strong fiscal period, you’ll need to record the transaction. There is nothing wrong with this procedure, except that a closing entry must be made to close the Dividends Declared account into Retained Earnings. As a result of this entry, the ultimate effect is to reduce retained earnings by the amount of the dividend. When recording the declaration of a dividend, some firms debit an account entitled Dividends Declared instead of debiting Retained Earnings. Returning to the General Electric Company example, the company paid dividends of $852 million in 1983, which represented 42% of its net income.

What are Dividends Payable?

After the distribution, the total stockholders’ equity remains the same as it was prior to the distribution. The amounts within the accounts are merely shifted from the earned capital account (Retained Earnings) to the contributed capital accounts (Common Stock and Additional Paid-in Capital). The difference is the 3,000 additional shares of the stock dividend distribution. The company still has the same total value of assets, so its value does not change at the time a stock distribution occurs. The increase in the number of outstanding shares does not dilute the value of the shares held by the existing shareholders.

Journal Entries for Dividends (Declaration and Payment)

The market value of the original shares plus the newly issued shares is the same as the market value of the original shares before the stock dividend. For example, assume an investor owns 200 shares with a market value of $10 each for a total market value of $2,000. Instead, the company prepares a memo entry in its journal that indicates the nature of the stock split and indicates the new par value. The balance sheet will reflect the new par value and the new number of shares authorized, issued, and outstanding after the stock split. To illustrate, assume that Duratech’s board of directors declares a 4-for-1 common stock split on its $0.50 par value stock.

Capitalization of Shareholder Loans to Equity

When a company declares a stock dividend, this does not become a liability; rather, it represents common stock the company will distribute to shareholders, so it’s reflected in stockholders’ equity. The company basically capitalizes some of its retained earnings, moving it over to paid-in capital. In this case, the journal entry at the dividend declaration date will not have the cash dividends account, but the retained earnings account instead. The company usually needs to have adequate cash and sufficient retained earnings to payout the cash dividend. This is due to, in many jurisdictions, paying out the cash dividend from the company’s common stock is usually not allowed. And of course, dividends needed to be declared first before it can be distributed or paid out.

Large Stock Dividends

While a company technically has no control over its common stock price, a stock’s market value is often affected by a stock split. When a split occurs, the market value per share is reduced to balance the increase in the number of outstanding shares. In a 2-for-1 split, for example, the value per share typically will be reduced by half. As such, although the number of outstanding shares and the price change, the total market value remains constant.

If you buy a candy bar for $1 and cut it in half, each half is now worth $0.50. The total value of the candy does not increase just because there are more pieces. Note that dividends are distributed or paid only to shares of stock that are outstanding. Treasury shares are not outstanding, so no dividends are declared or distributed for these shares. Regardless of the type of dividend, the declaration always causes a decrease in the retained earnings account. Stock investors are typically driven by two factors—a desire to earn income in the form of dividends and a desire to benefit from the growth in the value of their investment.

He has been the CFO or controller of both small and medium sized companies and has run small businesses of his own. He has been a manager and an auditor with Deloitte, a big 4 accountancy firm, and holds a degree from Loughborough University. Any net income not paid to equity holders is retained for investment in the business. The subsequent distribution will reduce the Common Stock Dividends Distributable account with a debit and increase the Common Stock account with a credit for the $9,000.

A reverse stock split occurs when a company attempts to increase the market price per share by reducing the number of shares of stock. For example, a 1-for-3 stock split is called a reverse split since it reduces the number of shares of stock outstanding by two-thirds and triples the par or stated value per share. A primary motivator of companies invoking reverse splits is to avoid being delisted and taken off a stock exchange for failure to maintain the exchange’s minimum share price. Many corporations issue stock dividends instead of, or in addition to, cash dividends.

Specifically, a company’s board of directors has declared a $1.20 per-share dividend on 1 December payable on 4 January to the common shareholders of record on 21 December. A high dividend payout ratio is good for short term investors as it implies a high proportion of the profit of the business is paid out to equity holders. However, a high dividend payout ratio leads to low re-investment of profits in the business which could result in low capital growth for both the business and investor. A long term investor might be prepared to accept a lower dividend payout ratio in return for higher re-investment of profits and higher capital growth. Assuming there is no preferred stock issued, a business does not have to pay a dividend, the decision is up to the board of directors, who will decide based on the requirements of the business. Dividend record date is the date that the company determines the ownership of stock with the shareholders’ record.

The maximum amount of dividends that can be issued in any one year is the total amount of retained earnings. A corporation can still issue a normal dividend (a dividend other than a liquidating one) even if it incurs a loss in any one particular year. This can be done as long as there is a positive balance in retained earnings. If there is a deficit (negative balance) in retained earnings, any dividend would represent a return of invested capital. Suppose a corporation currently has 100,000 common shares outstanding with a par value of $10.

Marketing Director at Kandy Zone,

Freelance Graphic Designer atTIGER'S,eYe and Executive Committee atThe Kandy Past Prefects Association, Past: Board of prefects' Vidyartha College Kandyand VIDYARTHA COLLEGE ,KANDY,SRILANKA.

Studies Cisco at Kandy SLIIT Promo

Past: Vidyartha College and Vidyartha College Astronomical Association

Lives in Kandy

From Kiribatkumbura, Sri Lanka · Moved toPilimatalawa

")

")