Both small and large stock dividends occur when a company distributes additional shares of stock to existing stockholders. Such dividends—in full or in part—must be declared by the board of directors before paid. In some states, corporations can declare preferred stock dividends only how to do a bank reconciliation: step-by-step process if they have retained earnings (income that has been retained in the business) at least equal to the dividend declared. The company can make the cash dividend journal entry at the declaration date by debiting the cash dividends account and crediting the dividends payable account.

Part 2: Your Current Nest Egg

The calculation can be done on a per share basis by dividing each amount by the number of shares in issue. Ask a question about your financial situation providing as much detail as possible. Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications. Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible. At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content.

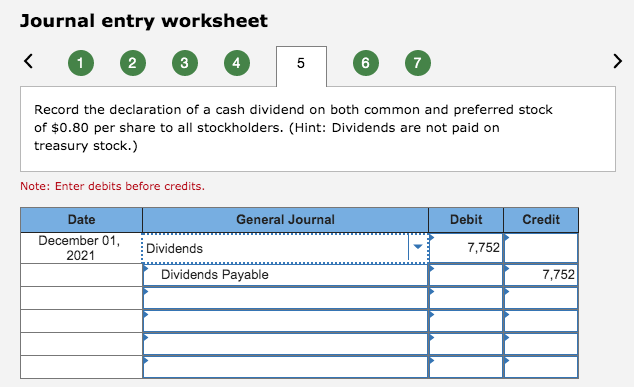

Journal Entries for Dividends (Declaration and Payment)

Clearly, a stock dividend conserves cash and thus allows the firm to use its cash for growth and expansion. That is, the current holders of stock receive additional shares of stock in proportion to their current holdings. Don’t worry, your balance sheet will still balance since there will be offsetting changes.

What are Dividends Payable?

The company makes journal entry on this date to eliminate the dividend payable and reduce the cash in the amount of dividends declared. Dividend is usually declared by the board of directors before it is paid out. Hence, the company needs to account for dividends by making journal entries properly, especially when the declaration date and the payment date are in the different accounting periods. A dividend is a distribution of a portion of a company’s earnings, decided by its board of directors, to a class of its shareholders. Dividends can be issued in various forms, such as cash payments, stocks or other securities. The board of directors determines the amount of the dividend, and the company must declare a dividend before it can be paid.

Do you own a business?

- Cumulative preferred stock is preferred stock for which the right to receive a basic dividend accumulates if the dividend is not paid.

- It is a temporary account that will be closed to the retained earnings at the end of the year.

- When the dividend is paid, the company’s obligation is extinguished, and the Cash account is decreased by the amount of the dividend.

- The company usually needs to have adequate cash and sufficient retained earnings to payout the cash dividend.

- The date of record establishes who is entitled to receive a dividend; stockholders who own stock on the date of record are entitled to receive a dividend even if they sell it prior to the date of payment.

(Both methods are acceptable.) The Dividends account is then closed to Retained Earnings at the end of the fiscal year. As you would expect, dividends shouldn’t impact the operating activities of your company. That means declaring, paying, and recording dividends won’t change anything on your income statement or profit and loss statement. Since shares of some companies can change hands quickly, the date of record marks a point in time to determine which individuals will receive the dividends. Accounting practices are not uniform concerning the actual sequence of entries made to record stock dividends.

Accounting for a Cash Dividend

Because there must be a positive balance in retained earnings before a normal dividend can be issued, the phrase “paying dividends out of retained earnings” began to be commonly used. On that date the current liability account Dividends Payable is debited and the asset account Cash is credited. If the corporation’s board of directors declared a cash dividend of $0.50 per common share on the $10 par value, the dividend amounts to $50,000. Dividends Payable is classified as a current liability on the balance sheet, since the expense represents declared payments to shareholders that are generally fulfilled within one year.

If there are more shares, then less money is distributed per share, and vice versa if there fewer shares outstanding. Many larger firms use a special checking account to disburse cash dividends. Again, in order to pay a cash dividend, a firm must have the necessary cash available, and the amount of cash on hand is not directly related to retained earnings. This journal entry is to eliminate the dividend liabilities that the company has recorded on December 20, 2019, which is the declaration date of the dividend.

The company pays out dividends based on the number of stock shares it has outstanding and will announce its dividend as a certain amount per share, such as $1.25 per share. When paying dividends, the company and its shareholders must pay attention to three important dates. As noted, this is often referred to as capitalizing retained earnings, because a portion of retained earnings becomes part of the firm’s permanent invested capital. In effect, after the stock dividend, each individual shareholder owns the same proportionate share of the corporation as he or she did before.

Buddika Roshan is the Co Founder at KandyZone. One of the main Photographer of the team. he studied at Vidyartha College, Kandy.

")